Krazy Times

By Rob Sigler, MBA

January 7, 2026

Economists are fond of talking about the economy as if it is a single monolithic force. They speak about the “American consumer” as being healthy, with increasing wages, wealth, and modest debt load. They note that the “American worker” is fully employed. They talk about a “manufacturing economy” that is stuck in neutral while remarking that the “service economy” remains quite healthy. They observe that consumption is strong and unemployment low. All of this belies the fact that there is no homogonous consumer or worker. Rather, the U.S. economy is an aggregation of different geographic influences, demographics, income cohorts, and economic sectors. What we find when we perform a more thorough forensic inspection is that the U.S. is presently trapped in a K-shaped recovery. What does that mean? Essentially, this phenomenon is defined as a bifurcated recovery where different groups experience dramatically different economic outcomes.

We see three imbalances affecting the U.S. economy and markets. First, higher income cohorts are driving the vast majority of wealth creation and consumption while lower cohorts are struggling. Second, while capital investment looks exceptionally robust, what we find is that a handful of technology names are engaged in an artificial intelligence (AI) spending frenzy that is making growth look stronger than it is. Third, while the stock market is screaming ahead with new 52-week highs frequently, it is being driven by a narrow group of companies. Said differently, lots of companies are lagging. Why should you care? We believe these imbalances are problematic and are apt to promote social strife, political upheaval, and insert volatility into market performance.

Let us first examine consumption trends. High-income earners feel very confident in their job prospects presently, have healthy wages, adequate savings, likely own their home with a very affordable mortgage, and have experienced very powerful gains in their wealth driven by strong stock market returns and home price appreciation. They are less impacted by unavoidable areas of inflation (food, healthcare, car insurance, and rent as examples) because it makes up a smaller proportion of their spending. By contrast, lower income households are feeling the pinch of inflation, face job insecurity, lack savings, likely are impacted by the resumption of student loan payments, and are facing higher-cost credit card debt. This group is finding housing unaffordable, cars difficult to finance, and bills hard to pay. So, when we look at the data, the differences are striking. The top 20% of U.S. earners are driving a touch over 60% of all consumer spending (Federal Reserve Bank of Dallas).

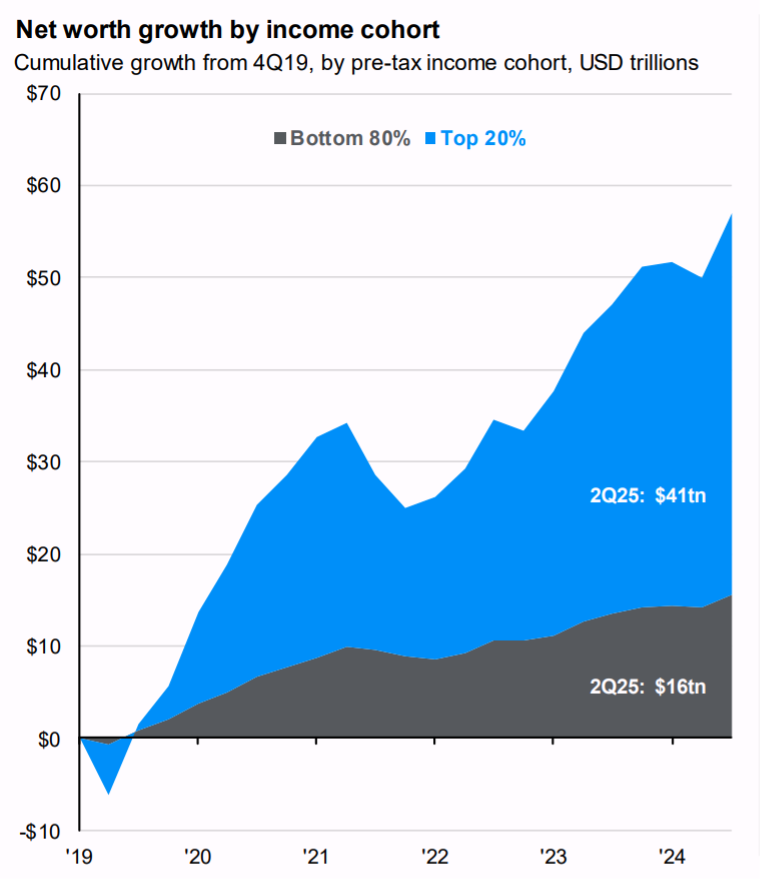

Closer examination of income trends indicates salary growth doesn’t appear to be the issue. Most income cohorts are averaging similar percentages. The real divide shows up in in the wealth effect. Simply put, lower income cohorts lack the asset pool that is providing the lift. How pronounced is this trend? The net worth of the Top 20% has risen by $41 trillion since the Pandemic initiation while the Bottom 80% has risen $16 trillion.

Thus, when we look at the aggregate consumer balance sheet on the left below, it looks quite healthy. Assets dwarf liabilities. However, the bifurcation shown above illustrates that most of the asset column belongs to higher income cohorts while a considerable piece of the liability side belongs to lower income cohorts. That is where the pain is being felt as household debt service climbs and delinquencies on auto loans, credit cards, student loans, and mortgages are rising.

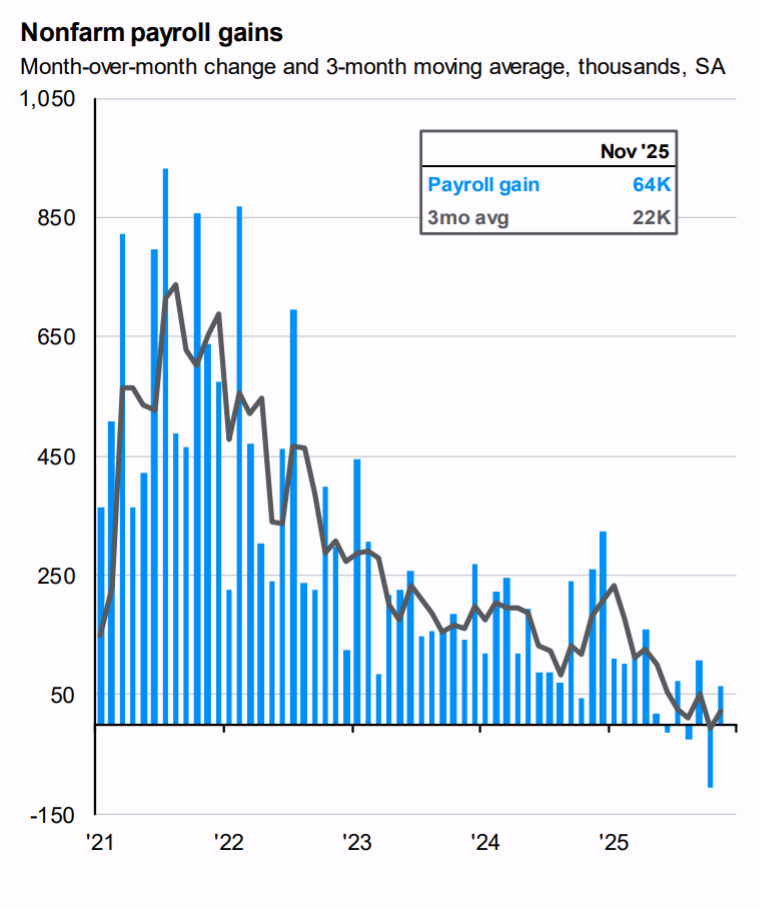

While this is occurring, the job market is weakening. Job growth is no longer keeping pace with labor force growth. Goldman Sachs estimates that the U.S. needs to create roughly 70k jobs per month to keep the unemployment rate steady. Unfortunately, we have fallen short of target in five of the last 7 months. Meanwhile, the unemployment rate has been on a steady rise, climbing from 4.1% in June 2025 to 4.6% in the latest November report. If this trend does not reverse, ultimately corporations will start to feel the pinch. They will lay off more workers and eventually the higher end consumer will retrench.

Meanwhile, there is another trend to watch. Politically, these imbalances are already driving some dramatic outcomes. Voters have elected a socialist-leaning mayors in New York City as well as Seattle. Democrats won gubernatorial races in Virginia and New Jersey and prevailed in special elections in Georgia, Iowa, Mississippi and Pennsylvania. Are these early election wins a signal of something bigger coming in the mid-terms? Could we see regime change usher in different tax policies (higher marginal rates, imposition of a wealth tax, change in capital gains treatment, changes in inheritance and gifting exemptions, corporate tax rate hikes)? Will we see rental controls, or other housing affordability initiatives? Could we see more unionization, rising minimum wages, expanded Social Security, etc.? The probability of all of this rises as the economic fortunes of different income strata diverge.

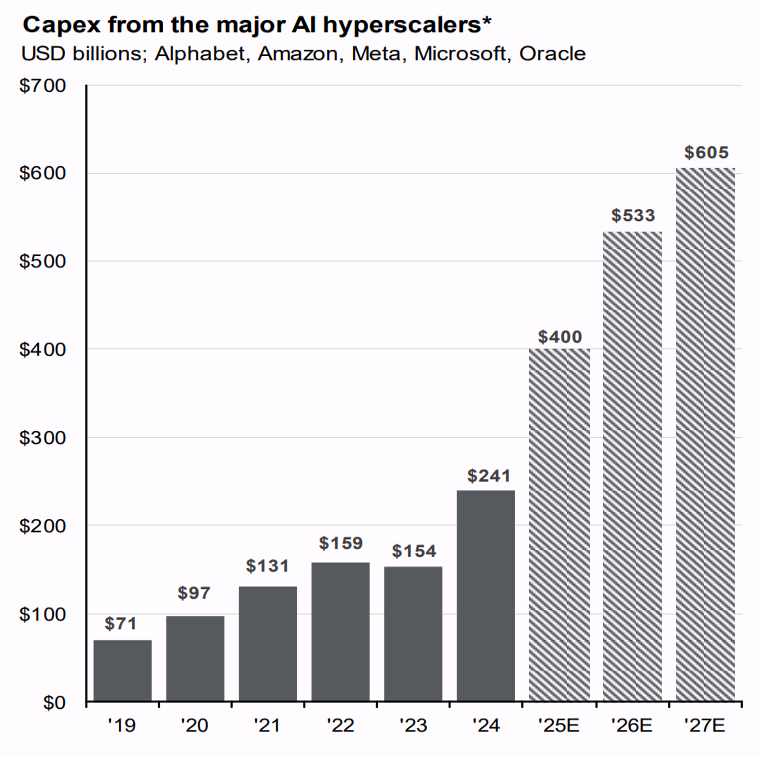

When we turn to capital investment, we see a feeding frenzy of spending in AI. Collectively over $1 trillion has been spent by five companies alone in the past five years. If forecasts prove accurate, that number could more than double in the next two years.

So, what is the problem you ask. Isn’t that a great thing? Keep in mind that business fixed investment has averaged roughly a 13% share of nominal GDP over the past 25 years. Just some rough math here, but if we have a $29 trillion economy and 13% comes from business fixed investment, that equates to about $3.7 trillion. As you look at the illustration above, five companies are expected to spend $533B in 2026. Of the $3.7 trillion pie, that represents 15% of the total. Realistic? Sustainable? The challenge that we foresee is that few companies are producing economic returns from their AI investment. The Bay Area Times reports the following examples. OpenAI (parent of ChatGPT) is expected to burn $9B of cash on $13B in sales this year. Anthropic (parent of AI engine Claude) is expected to burn $3B of cash on $4.2B of sales in 2025. Neither of these companies are expected to turn profitable until 2030. Meanwhile, much of the investment into AI is being financed by debt. What happens to capital investment if AI infrastructure spend turns out to have parallels with the Internet Bubble of 2000? In that situation, we dramatically overbuilt capacity and struggled for years to absorb it. Make no mistake, there is a bubble building in AI, it is simply a matter of when it bursts.

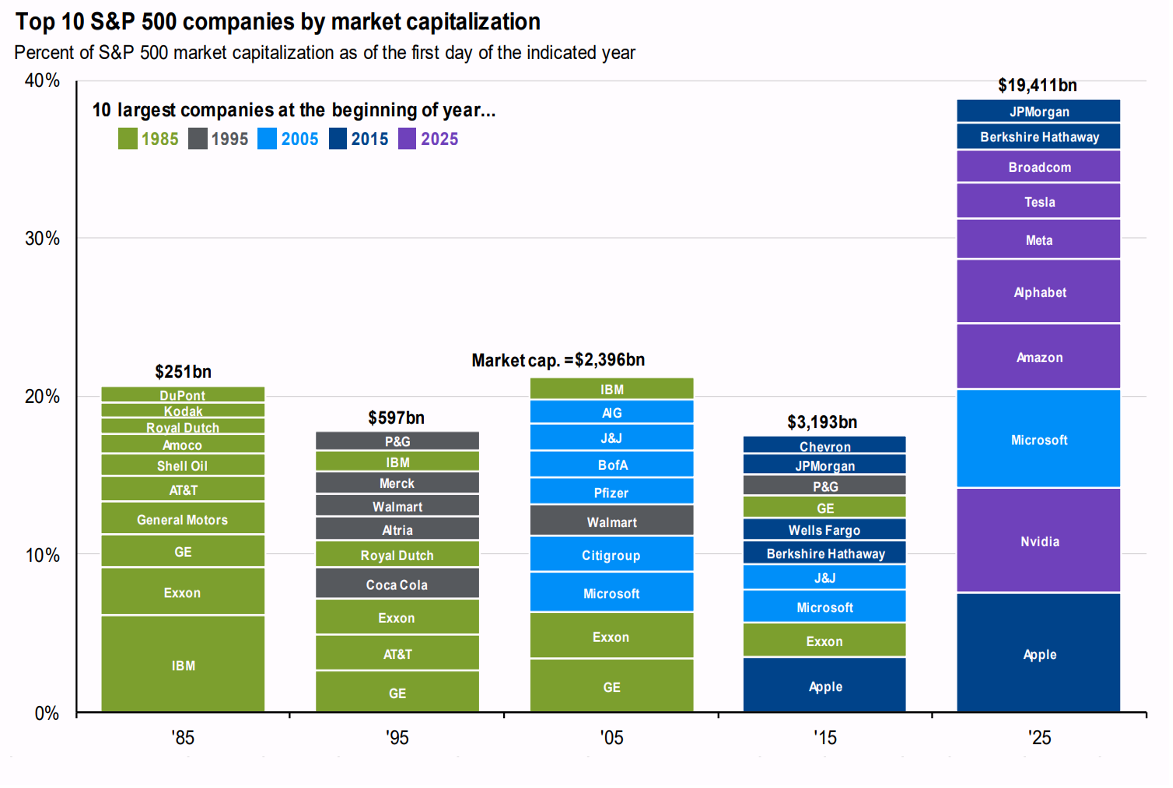

Finally, let’s turn the turret to market composition and returns. Interestingly, the stock market has taken on much the same complexion as the economy. Seven companies within the S&P 500 account for 36% of its market capitalization. They are collectively responsible for 50% of the growth in earnings for the entire index in 2025. Similarly, we see it in performance. While the market capitalization weighted S&P 500 index was up 17.75% in 2025, the equal weighted S&P 500 was up 11.22%. Said differently, the largest constituents in the S&P 500 index are driving the bulk of the returns. Much like the economy, the stock market is divided into haves and have nots. Technology firms at the heart of the AI capital expenditure cycle are the engine of market strength. Again, this begs the question of why is this a problem? At the moment, it isn’t. However, history tells us that market dominance is typically fleeting. The following illustration shows the largest companies in each of the past five decades. What you will see is that change is constant. However, unlike the previous four decades when the top ten companies represented roughly 20% of market capitalization, the top ten companies have ballooned to roughly 40% of the index today. Said differently, more of your eggs are in the same basket.

In closing, we believe our paramount responsibility at Westshore Wealth is to steward our clients’ capital responsibly through all seasons of market volatility. To successfully accomplish that mission, we need to constantly surveil hazards, as we have attempted to do above. Our assessment leads us to believe that the resting temperature of market risk is rising. Please don’t misunderstand. We are not calling for a massive crash or correction. We don’t want our clients to use this as a siren call to raise cash. The Dot.Com bubble built for nearly three straight years before correcting. The housing bubble was evident for years before the collapse in 2007-08. Rather, it simply means now is the time to follow Warren Buffett’s advice. Namely “be fearful when others are greedy.” How do we do that? History tells us that no one can consistently time the market. We agree, adhering to the adage that time in the market, not timing the market, is the key to superior returns. So, you will not see us rush to cash. We believe the best risk mitigation is accomplished through portfolio composition and positioning.

As we enter 2026, we believe a more cautious approach to 2026 is warranted. We intend to ramp up our usage of shock absorbers in the portfolio. We believe the setup for domestic equities will get more challenging with elevated valuations and sky-high expectations regarding AI contribution. We believe international and emerging markets will continue to outperform domestic equities given the weakening dollar and we have positioned accordingly. In fixed income, we believe rising unemployment levels, in concert with lapping of tariffs, will cause inflation concerns to fade and usher in better returns. We also see the odds as high that the Supreme Court strikes down Trump’s usage of wartime powers to impose tariffs. This may create some heightened volatility, however, it should ultimately free up the Federal Reserve to be more aggressive with interest rate accommodation. Finally, we continue to favor heavy contributions towards uncorrelated diversifiers like triple net lease real estate, private infrastructure, distressed debt, and private equity.

We welcome your questions and wish you a Happy New Year!

About the Author

Robert Sigler, MBA

Rob serves as a Managing Director and the Chief Investment Officer for Westshore Wealth. Rob’s long career in the financial services industry reflects a diverse set of vocational tools and experience. He has advised some of the world’s most renowned […]

Learn More