Participation Paradox

By Rob Sigler, MBA

May 6, 2026

A paradox is a situation that seems to contradict itself or defy common sense, yet upon investigation, reveals itself to be true. Much of what has transpired in the equity market qualifies. Since the commencement of hostilities with Iran just over 60 days ago, oil and gasoline prices have risen roughly 50%, U.S. consumer confidence plunged to an all-time low in April (U. of Michigan Final Sentiment Index), inflation pressures intensified and hopes for easing monetary policy by the Federal Reserve have been dashed. That said, April 2026 witnessed one of the most historic rallies in market history. The S&P 500 Index rose 10.4% and experienced a 12% gain in just 13 days to start the month. That has only happened nine other times in history. While other such occurrences generally coincided with deeply depressed equities markets bouncing off the bottom, this episode was different. In this circumstance, U.S. equities trade near the 100th percentile in terms of observed valuations (meaning the top of the high end). This latest equity rally propelled us to new all-time highs. Does it make sense?

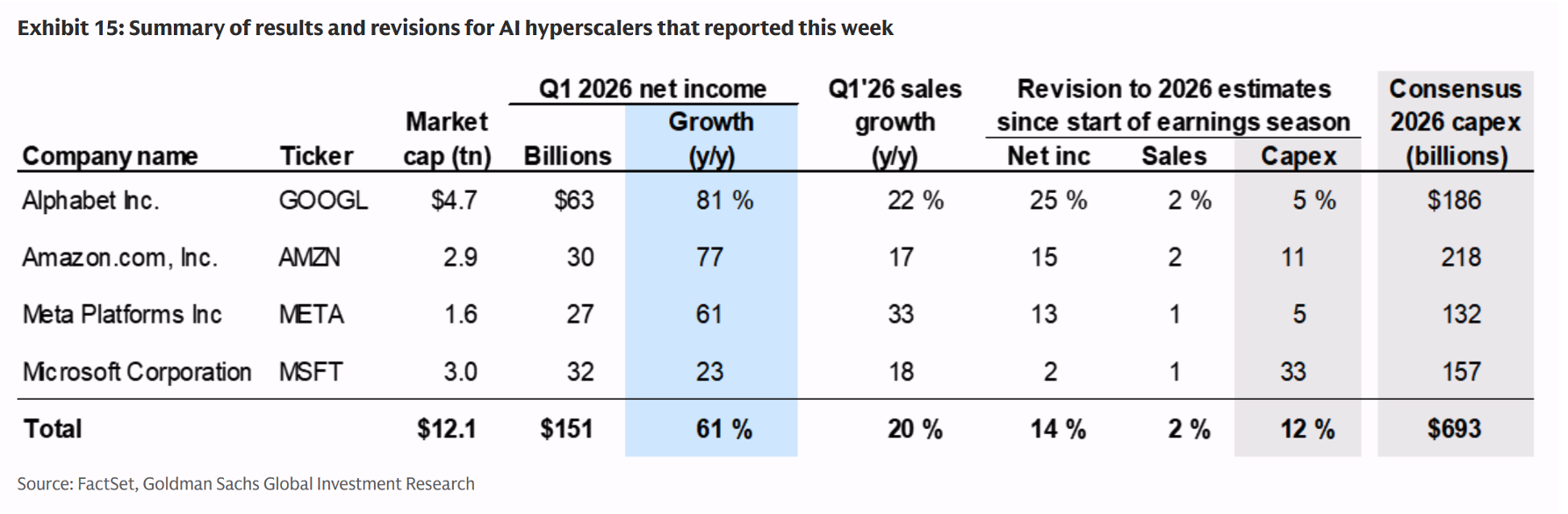

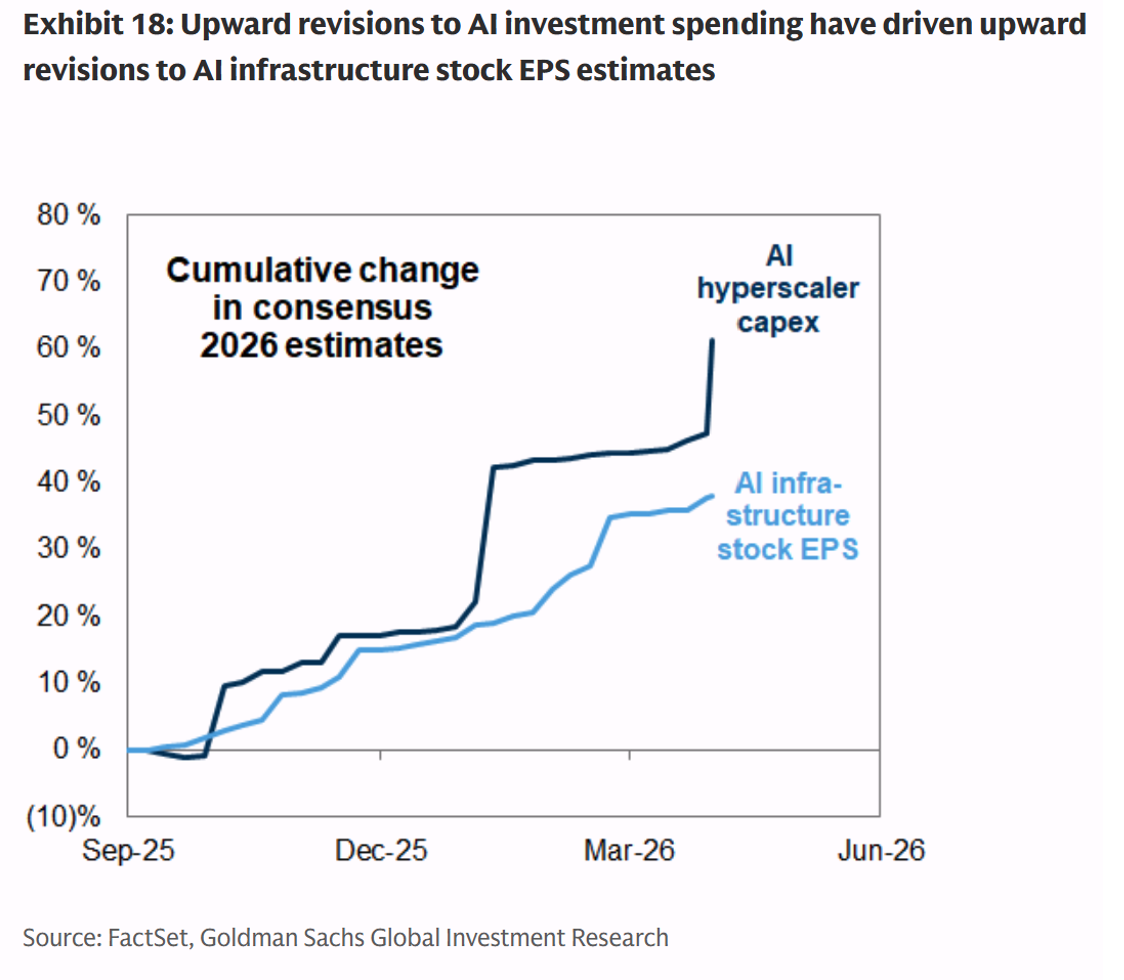

In our estimation, the reaction was rational. The stock market is taking its cues from several key factors. First, at Westshore we continue to argue that geopolitical risk events are to be bought, not sold. Our analysis of more than 30 such events since 1939 suggests that the equity market typically sells off sharply upon initiation (on average 7.6%), reaches bottom on average roughly 16 days hence, and typically recovers 12.2% from the bottom twelve months later. Thus, we see this incident playing out entirely to script. Second, the market is laser focused on the benefit of fiscal stimulus measures passed last year in the One Big Beautiful Bill Act (OBBBA). The key provisions increased tax refunds by approximately 30% and spurred capital expenditure by offering companies the tax benefit of accelerated depreciation. Thus, while gasoline costs are impacting consumer wallets, tax refunds provide a powerful salve. Third, the Artificial Intelligence (AI) driven capex cycle is positively massive. The U.S. Hyperscalers (Amazon, Google, Meta, Microsoft) alone are spending nearly $700 billion this year. Total AI investment is closer to $1 trillion. To put that in context, that is almost 3% of U.S. Gross Domestic Product.

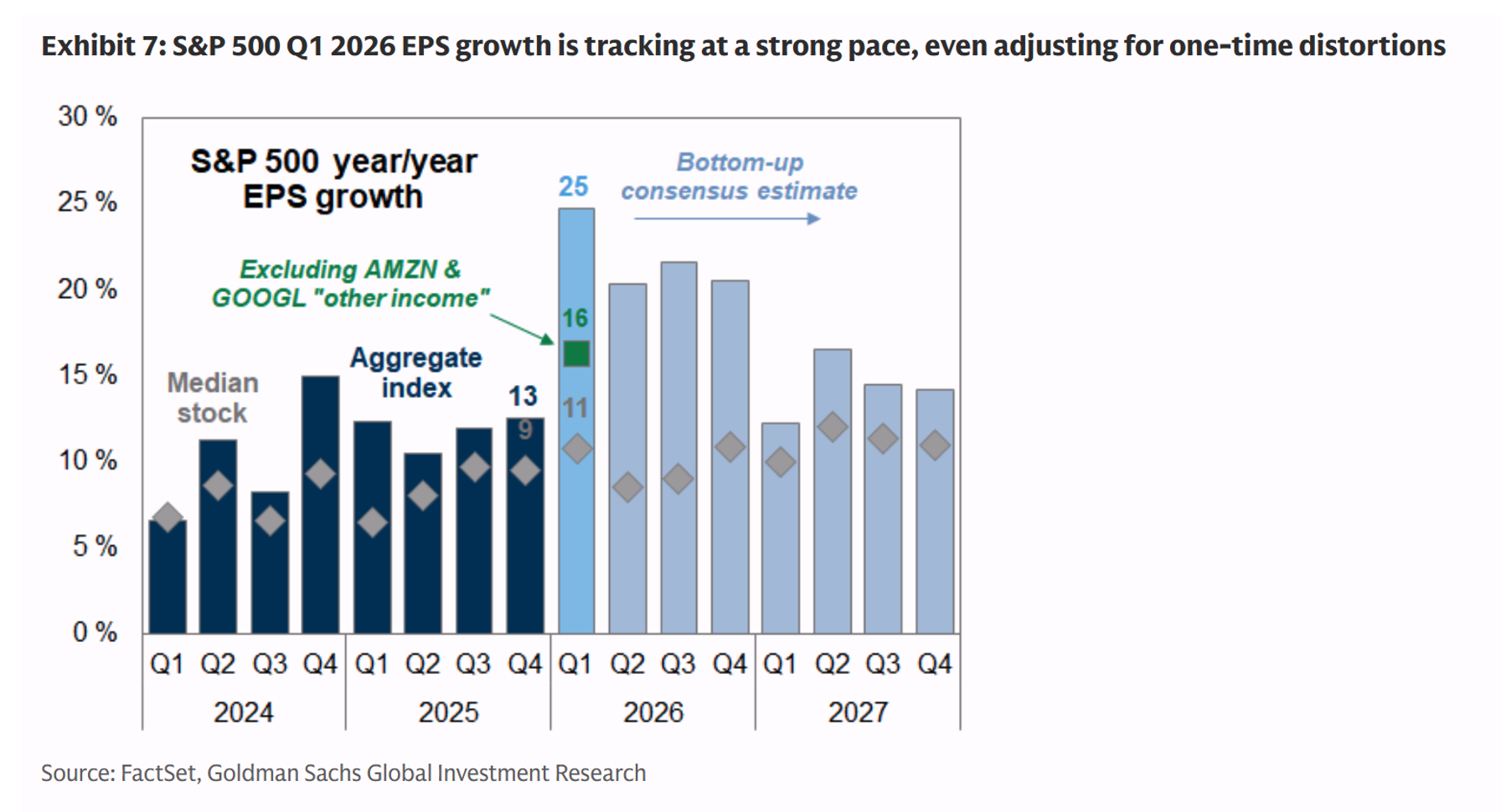

That brings us to the final point. This is providing a massive tailwind to corporate earnings. Semiconductors, one of the key building blocks to the data center build, saw earnings accelerate by nearly 90% in the present quarter. Meanwhile, broader technology saw earnings grow 40%. Expanding the scope, with roughly 63% of S&P 500 companies reporting thus far in 1Q26, earnings are tracking up 16% (adjusting for one-time items) according to Goldman Sachs.

This is the strongest quarterly earnings growth since 2021. Furthermore, earnings revisions for the remainder of 2026 have been rising rapidly. Thus, the reasons behind the equity move make sense to us and we don’t want to lose sight of these positives.

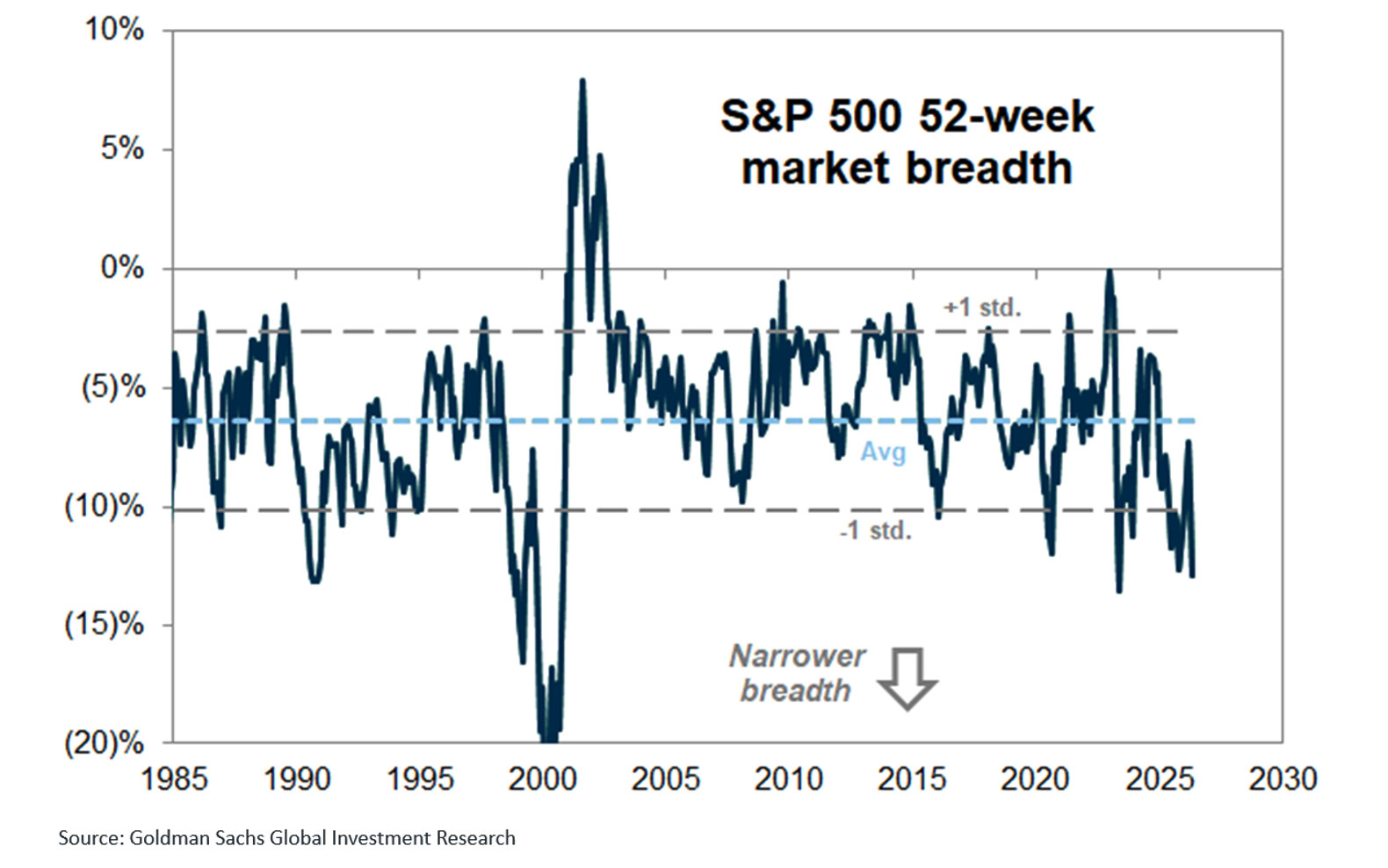

However, as our title revealed, with any paradox there is an opposing truth that exists as well. This market is not overwhelmingly healthy. It suffers from what market technicians refer to as bad breadth. What does that mean in plain English? It means that the S&P 500 Index performance is not particularly representative of the average stock. For example, while the S&P 500 index has rallied 14% since its 52-week low in March, and trades at a record high, the median constituent in the S&P 500 remains 13% below its respective high. We haven’t seen this kind of divergence since the Dot-Com Bubble.

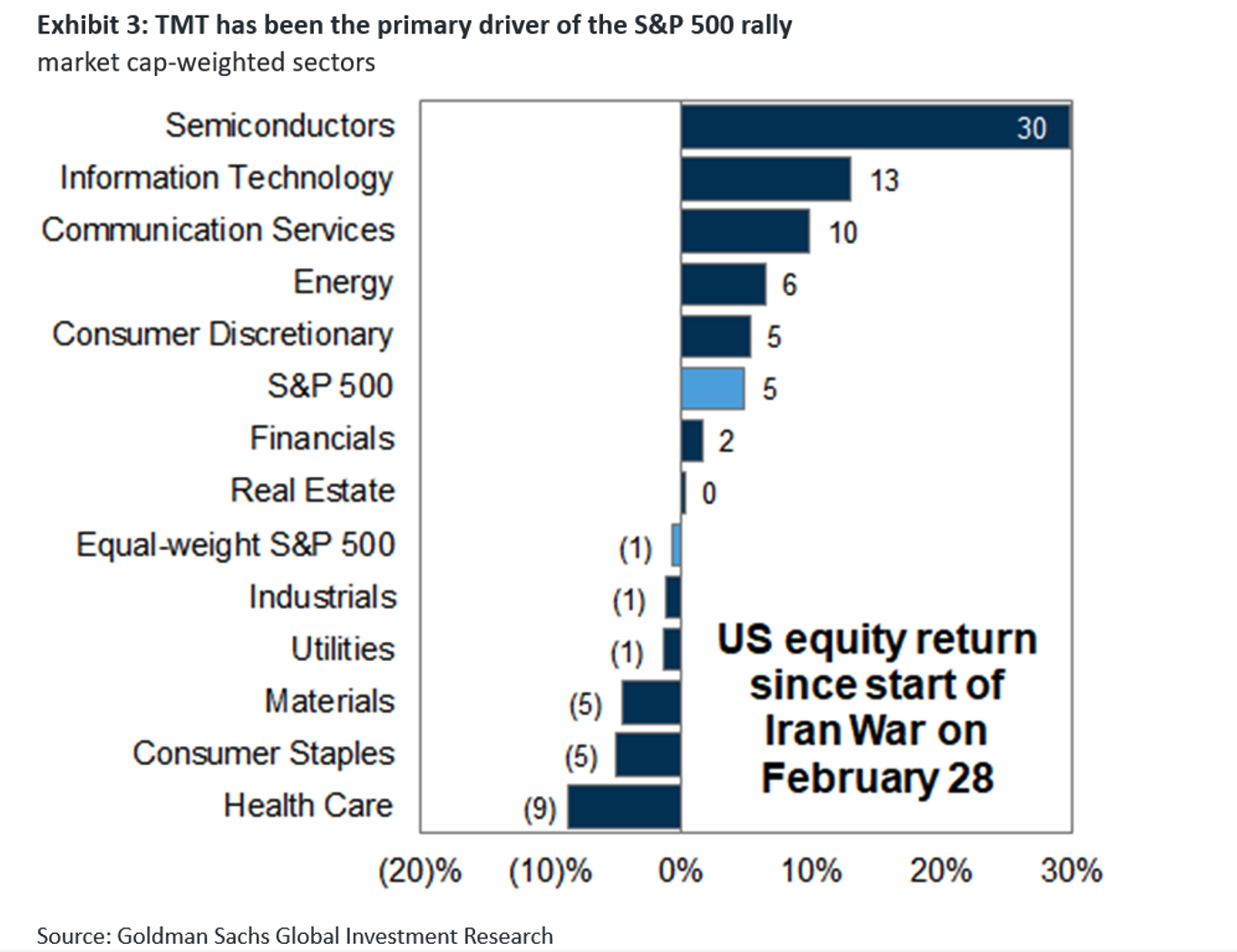

Furthermore, when we look at what has propelled the market, we find that it is very linked to AI related infrastructure build. Six sectors have registered gains since the start of the Iran War, while five sectors are negative. Not surprisingly three of these are related to technology and the fourth are energy stocks that are being propelled by rising commodity prices.

While narrow breadth can persist for months, it always resolves itself with a leadership rotation. The direction can be negative or positive. In the “catch down” scenario, recent market leaders fall, while a “catch up” scenario sees recent laggards recover. Which will happen this time? Our sense is that the momentum of the AI cycle is ultimately going to slow. Much like the telecom equipment boom associated with the Internet Bubble of 2000, we believe there will be a digestion phase after this massive capital expenditure boom slows. However, we don’t believe that will happen soon. Judging by recent commentary from technology company conference calls, capex is likely to remain elevated for some time to come.

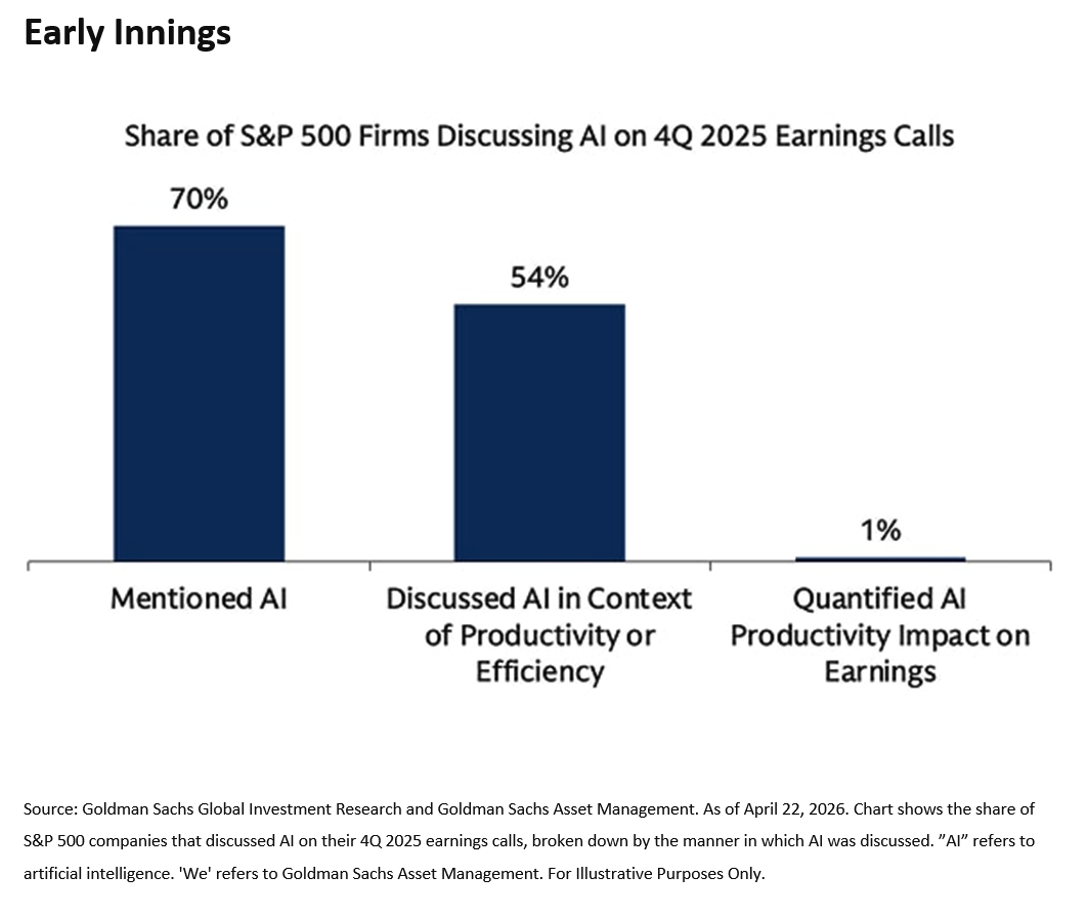

Where does that leave us? Bottom line, the participation paradox pits the positive trends of corporate earnings against the reality that AI investment will eventually slow. Investors will start to demand a return on all that investment. Right now, we are building the infrastructure. That involves a huge amount of investment in semiconductors, servers, data networking equipment, telecom equipment, memory, power, and physical building to name a few. Additionally, all of these require the inclusion of a massive amount of basic materials as their building blocks. However, the reality of AI delivering actual productivity, meaning increasing output while decreasing human capital, appears to still be in its infancy. Case in point, during the 4Q25 earnings season, roughly 70% of S&P 500 companies referenced AI during conference calls, but only 1% qualified a boost to earnings from AI productivity gains.

Eventually, we will have enough infrastructure. We will need the application layer on top of this to deliver on the promise of AI. What does that mean? Remember, the internet was a massive, decentralized system of interconnected computer networks that allowed standardized protocols for information sharing. It was invented in 1983. AOL came around in 1989. Google allowed people to search, find, and obtain information with its founding in 1998 nine years later. Amazon was founded in 1994 but didn’t expand beyond online book sales until 1998 and only became a broader marketplace in 2000. Netflix didn’t offer streaming content until 2007. Our point here is that eventually the bulk of the infrastructure build will be behind us. That massive earnings boost to corporate earnings will fade. The application layer is what will deliver the use cases for AI to drive the next revenue and earnings opportunity. Will that transition happen gracefully? It is very hard to handicap at this point.

Thus, at Westshore, we are taking a measured approach. We want to be involved to capture the upside. That said, we are operating with eyes wide open to the fact that the market is very narrow and susceptible to pullback if these primary themes start to slow. That latter issue has us continuing to allocate towards equities while simultaneously embedding shock absorbers into our exposure (using structured notes and buffered ETF exposure as examples). Additionally, we are populating a significant sleeve of alternatives (private equity, asset backed credit, infrastructure, triple net lease real estate and distressed debt as examples) that tend to act as uncorrelated diversifiers in portfolios and dampen risk in the long term. We think this “halfway in” portfolio construction approach grants us the ability to capture solid returns while keeping us adequately nimble to pivot if conditions change.

We welcome your questions.

About the Author

Robert Sigler, MBA

Rob serves as a Managing Director and the Chief Investment Officer for Westshore Wealth. Rob’s long career in the financial services industry reflects a diverse set of vocational tools and experience. He has advised some of the world’s most renowned […]

Learn More